The daily brief starts with a 20-second read. The deeper sections are optional. |

📌 20-SECOND BRIEF

• Regime: S&P 500 7,600 🔺 and Nasdaq RSI 79 🔺 show momentum still alive, but participation is not broad.

• Core Gap: Polymarket (prediction markets that price real-money probabilities) assigns 69% odds to zero Fed cuts in 2026 🔻 while growth equities still behave like policy relief is nearby.

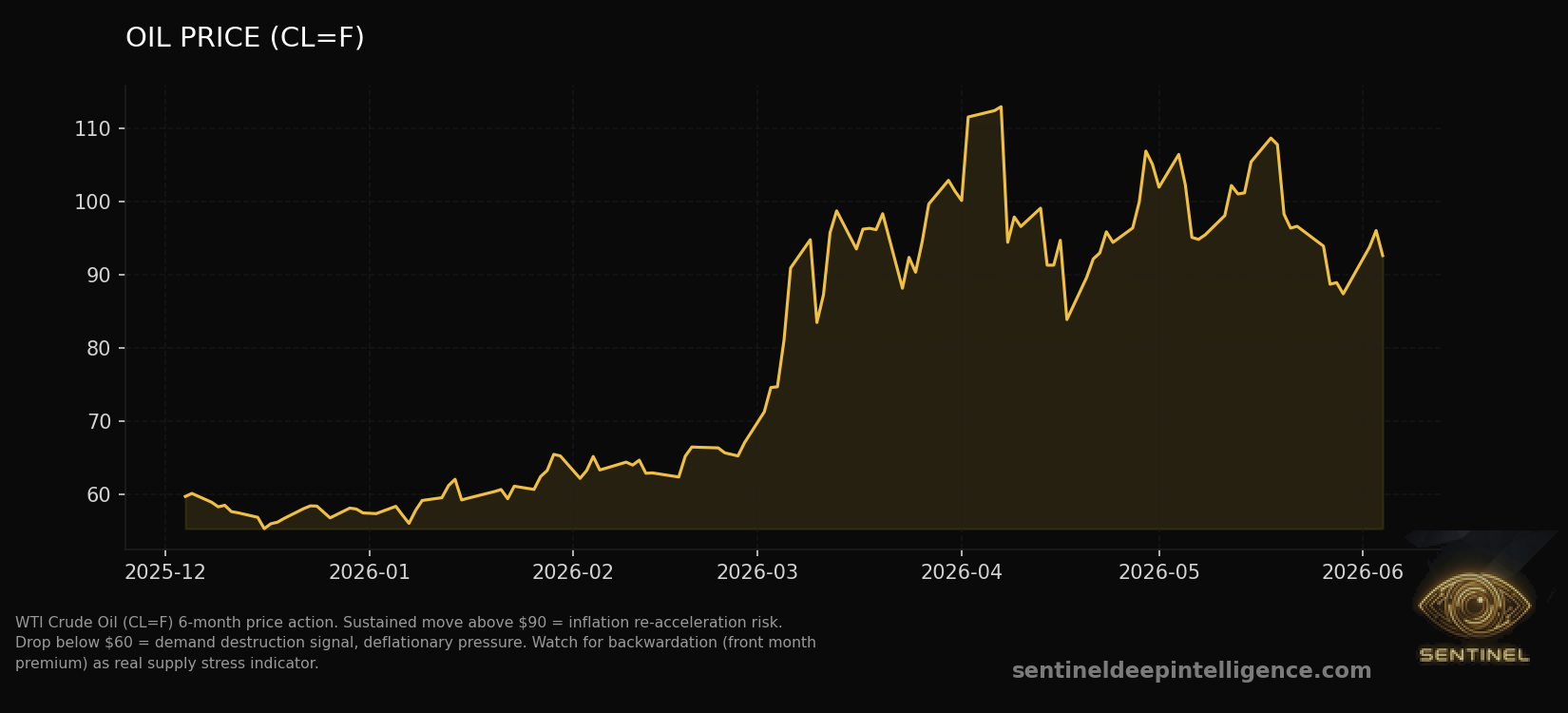

• Catalyst: Crude oil at $91 🔺 keeps the inflation channel open even as headlines lean on ceasefire language.

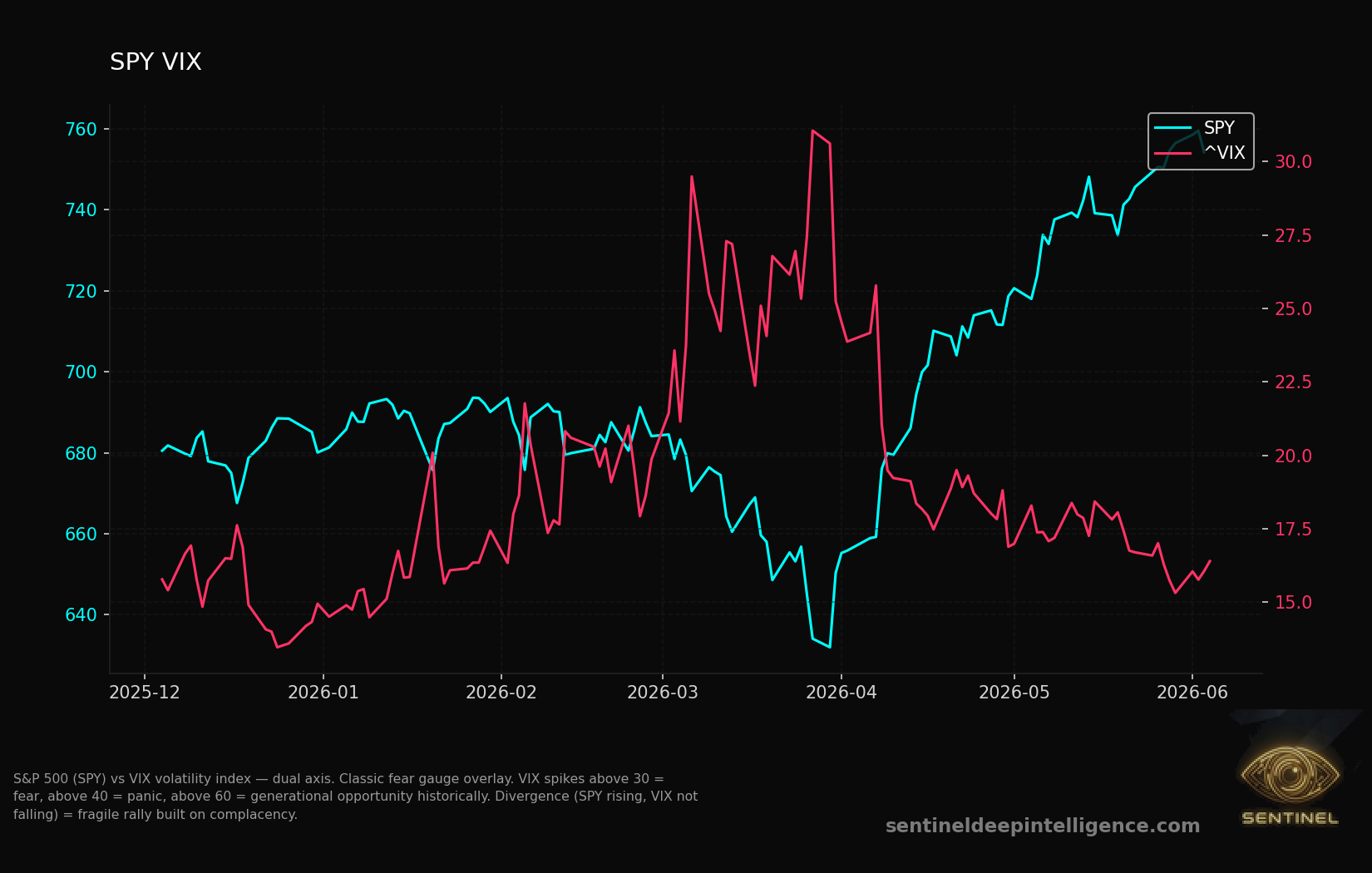

• Watch: Breadth 53% 🔻, VIX 16 🔺, and DIX 41.7% 🔻 decide whether this remains controlled or starts repricing. |

KEY CHARTS   |

WHAT CHANGED 01 - Oil stopped being background noise. Crude is now $91.28 🔺 after yesterday's near-$90 tape. Prediction markets price crude above $84 in June at 60% on $208K volume, which means the market is not treating the energy shock as finished.

02 - The Fed cushion got thinner. Polymarket prices zero 2026 cuts at 69% on $31.3M volume and July no-change at 92% on $7.2M. The crowd is watching AI headlines, but the policy market is quietly removing the spare tire.

03 - Surface strength narrowed. Nasdaq rose 0.60% 🔺 and S&P rose 0.26% 🔺, while Russell 2000 slipped 0.47% 🔻 and breadth sits at 53%. This is leadership, not full market participation. |

THE CORE READ The market is not panicking. It is compartmentalizing. Equities are accepting AI momentum, high dealer gamma, and low VIX as permission to keep climbing, while oil and policy markets are pricing a less forgiving macro backdrop.

That matters because expensive growth can survive high rates when liquidity is generous, or survive energy stress when the Fed is flexible. Today, neither side of that safety net is obvious. This is a calm tape with a cost-of-capital problem under the floorboards. |

🗺️ SCENARIO MAP - 5-15 trading days

Base Case - 45%

Equities stay controlled, VIX remains below 18, and GEX keeps intraday moves dampened. Oil stays elevated but does not accelerate enough to dominate earnings or inflation headlines.

Downside Repricing - 35%

Oil holds above $90, breadth breaks below 50%, and DIX stays near 42% or lower. In that path, the market stops treating energy as a headline and starts treating it as a margin tax.

Relief Extension - 20%

Oil moves back below $88, breadth stabilizes above 55%, and AI leadership broadens beyond the same handful of names. That would delay the repricing risk and restore a cleaner risk-on tape. |

|